With larger batteries and faster charging becoming common, the need for advanced monitoring and control – Battery Management System – has become even more critical.

The electric vehicle story is often told through sleek designs, longer driving ranges and faster charging times. But behind all of this, there is a silent system working every second to keep everything running safely and efficiently. This is the battery management system, or BMS—and today, it is becoming one of the most critical technologies shaping the future of mobility.

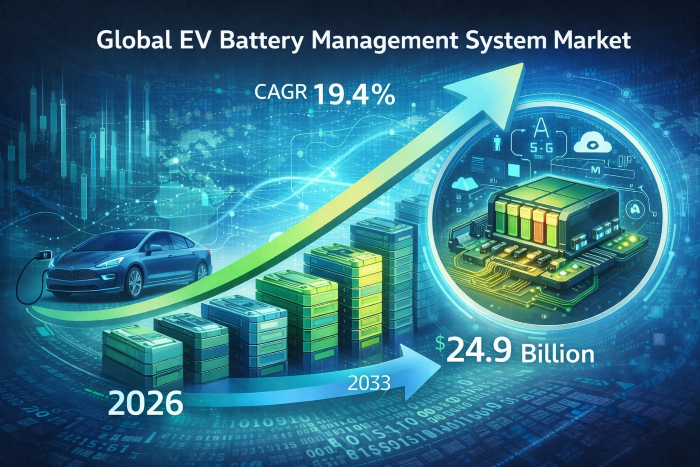

The market for these systems is growing rapidly. From about $7.2 billion in 2026, it is expected to reach nearly $25 billion by 2033. This sharp growth reflects a simple reality—without a strong and intelligent BMS, an electric vehicle cannot perform reliably. These systems monitor battery health, control temperature, manage charging and ensure safety. In many ways, they act as the brain of the vehicle.

According to Persistence Market Research, a leading management consulting firm, this rising importance is closely linked to the global shift towards electric mobility. Governments are pushing for cleaner transportation through stricter emission norms and incentives. As a result, EV sales are rising across the world, from passenger cars to buses, trucks and two-wheelers. With larger batteries and faster charging becoming common, the need for advanced monitoring and control has become even more critical.

At the same time, technology is changing what a BMS can do. Earlier, these systems were mainly focused on basic monitoring. Today, they are becoming intelligent platforms. With the integration of artificial intelligence, IoT and cloud connectivity, BMS can now predict battery behaviour, detect issues early and optimise performance in real time. This is especially important for fleet operators, where battery efficiency directly affects costs and uptime.

A major shift is also happening at the hardware level. New innovations, such as advanced chipsets with built-in diagnostic capabilities, are making it possible to monitor battery health more accurately from inside the vehicle itself. This means problems can be detected earlier, safety can be improved, and battery life can be extended without relying on external testing.

The report noted that the market structure itself is evolving. Simpler, centralized BMS systems continue to dominate because they are cost-effective and easy to integrate, especially in passenger vehicles. But modular systems are growing faster, particularly in commercial vehicles and larger battery applications. These systems offer flexibility, better fault management and easier scaling, which are becoming important as EV platforms diversify.

Asia Pacific Leads the Market

Geographically, Asia-Pacific remains at the centre of this growth, driven by strong EV production and battery manufacturing in countries like China, Japan and South Korea. India is also emerging as a key player, especially in software and engineering capabilities. Meanwhile, North America is growing quickly with strong policy support and investments, and Europe continues to lead with strict regulations and advanced technology adoption.

Centralised Systems Lead Market Share

The centralised BMS topology holds the largest market share, accounting for approximately 47%, supported by its simple architecture, lower cost, and ease of integration into passenger electric vehicles with moderate battery capacities. Its single control unit design streamlines monitoring and supports compliance with functional safety standards such as ISO 26262, making it widely adopted among mass-market EV manufacturers. The modular BMS architecture is the fastest-growing segment, driven by rising demand in electric buses, commercial vehicles, and high-capacity battery systems that require scalability and enhanced fault isolation.

Modular designs enable flexible configurations, easier maintenance, and improved thermal management across large battery packs. A notable development in this segment is the increasing adoption of modular BMS platforms by OEMs to standardize battery systems across multiple EV models, reducing redesign efforts and accelerating time-to-market. This shift reflects the industry’s move toward more adaptable and high-performance battery management solutions aligned with next-generation EV requirements, the report mentioned.

The competitive landscape is equally dynamic. Global players are investing heavily in innovation, partnerships and digital capabilities. The focus is clearly shifting towards smarter, connected and safer battery systems that can support the next generation of electric vehicles.

Key Players and their Business Strategies

Leading players in the EV battery management system market include Robert Bosch GmbH, Continental AG, Denso Corporation, LG Energy Solution, NXP Semiconductors, Texas Instruments, and Mitsubishi Electric Corporation, among others.

Bosch focuses on advanced BMS platforms with integrated software and connectivity features to enhance battery efficiency, while Aumovio (formerly Continental AG) emphasises scalable solutions tailored for electric and hybrid vehicles. On the other hand, Denso Corporation invests in high-precision battery monitoring technologies for improved safety and performance. NXP Semiconductors and Texas Instruments lead in semiconductor innovation, enabling smarter and more efficient BMS architectures. LG Energy Solution leverages its battery manufacturing expertise to deliver integrated battery and management systems.

Key strategies across the market include partnerships, technological innovation, and expansion of production capabilities. Companies are prioritising digital integration, predictive analytics, and compliance with evolving safety standards.

In many ways, the future of electric mobility will depend not just on better batteries, but on better ways to manage them. And as vehicles become more intelligent and connected, the role of battery management systems will only become more central—quietly ensuring that the EV revolution moves forward safely, efficiently and at scale.

NB: Illustration is representational; report courtesy: Persistence Market Research.